Why I Am Writing About Stocks in Public

I have kept plenty of investing thoughts private. That made the process easier, but not necessarily better.

Private notes let me change the story after the fact. I can remember the clean version of the thesis, forget the part I was unsure about, and pretend the outcome was more obvious than it was. Public writing makes that harder. It turns investing into a record instead of a feeling.

So I am going to write about stocks here.

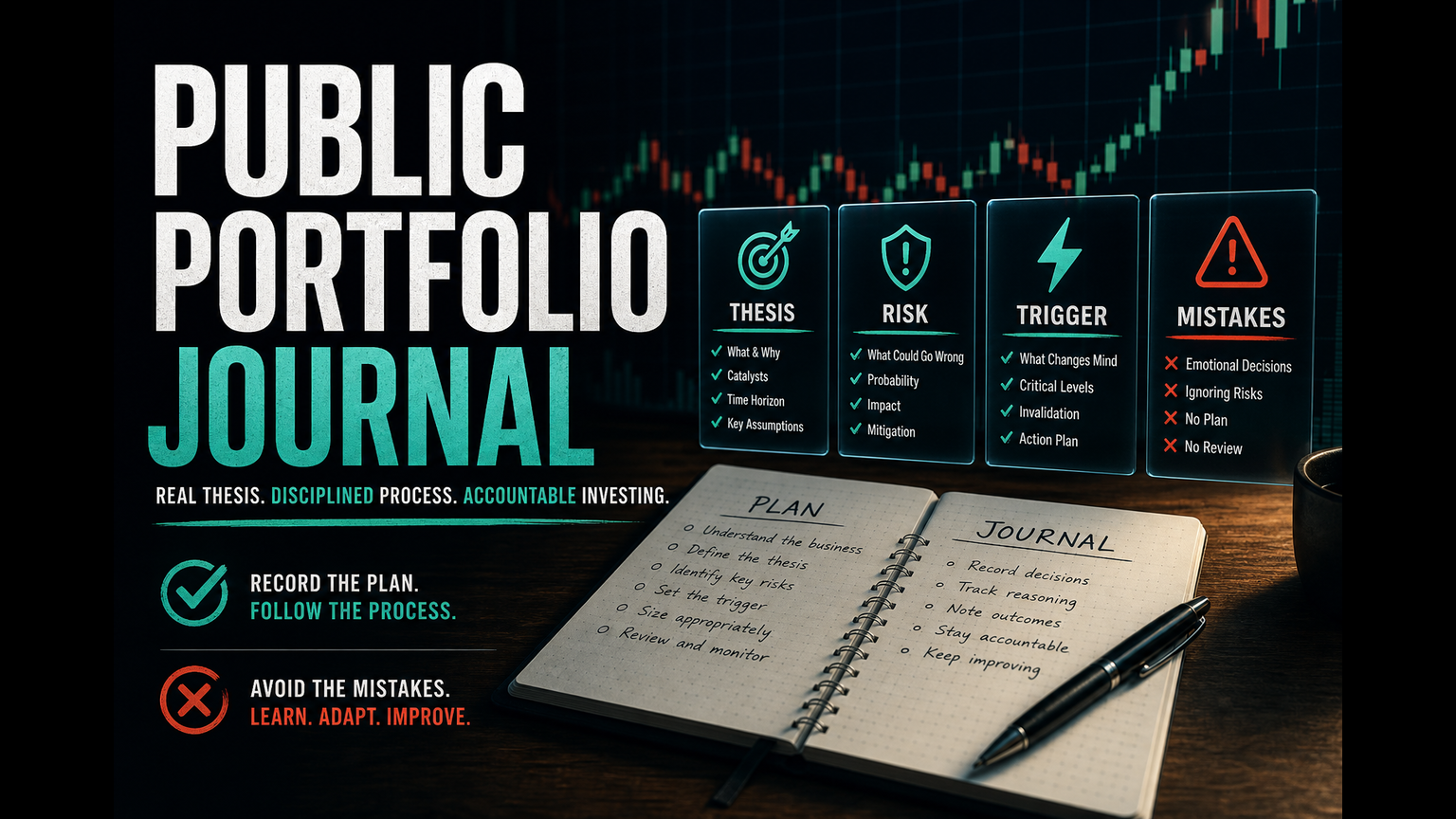

Not as advice. Not as a guru act. Not as a performance scoreboard. This is a personal portfolio journal: what I am looking at, what I own or choose not to own, what I believe at the time, and what would make me change my mind.

Nothing here is financial advice. I am writing for my own clarity in public.

Why public

The useful part of public writing is not attention. It is accountability.

When I write down a stock thesis before the result is known, I have to name the actual bet. Is it revenue growth? Margin expansion? Multiple compression already priced in? A management team I trust? A product cycle I think the market is underrating? A balance sheet that gives the company time?

Those details matter because they create falsifiable memory. Later, I can compare the world I expected with the world that arrived.

That is the same reason I write about software. Writing is how I stress-test ideas. Shipping is how I stress-test intuition. Investing adds another version of the same discipline: capital forces a decision, and the market eventually grades whether the reasoning had any edge.

What I will write down

I want each portfolio note to capture the decision, not just the ticker.

That means the thesis, the risks, the time horizon, the position sizing logic when I am willing to share it, and the trigger that would make me revisit the view. I also want to record what I am deliberately ignoring. Every investment has noise around it. If I do not say what I am filtering out, I can always pretend later that the noise was part of the plan.

The goal is not to be right in every post. The goal is to make the reasoning inspectable.

If a position works, I want to know whether it worked for the reason I believed. If it fails, I want to know whether the thesis broke, the timing was wrong, or I simply paid the wrong price. Those are different mistakes. Treating them as one vague category is how you avoid learning.

What this will not become

This will not become a feed of hot takes.

Markets reward patience more often than commentary. I am less interested in reacting to every move than in building a record of decisions I can return to. Sometimes that will mean writing about a company. Sometimes it will mean writing about process: valuation, position sizing, cash, concentration, or the emotional mistakes that show up when money is involved.

I also do not want to perform certainty. The point of a journal is to preserve the uncertainty that existed at the time. If I write with too much confidence, the record becomes less useful.

The standard I want is simple: make the thesis clear enough that future me cannot hide from it.

That is the reason to write about stocks in public. Not because public writing makes the portfolio better by itself, but because clear records make bad reasoning harder to excuse.